Elasticity of Demand: A measure of how consumers react to a change in price

Elastic demand

1.demand that is very sensitive to a change in price

2.product is not a necessity

3.there are available substitutes

4.always greater than 1

ex. soda/steak/fur coat

Inelastic demand

1.demand that is not very sensitive to a change in price

2.product is a necessity

3.little to no substitutes

4.always less than 1

ex. gas, insulin

Unitary elastic

Perfect society/always equal to 1

Total revenue: total amount of money a company receives from selling goods and services

Price x Quantity = Total revenue

Marginal revenue: additional income from selling one or more unit of a good

Fixed cost: it is a cost that does not change no matter how much of a good is produced

Variable cost: it is a cost that rises or falls depending upon how much is produced

TFC + TVC = TC

AFC + AVC = ATC

TFC/Q = AFC

TVC/Q = AVC

TC/Q = ATC

AFC x Q = TFC

AVC x Q = TVC

Marginal cost = new TC - old TC

output = quantity

Equilibrium: point at which the supply curve and demand curve intersect

Excess Demand: where quantity demanded is greater than quantity supplied (shortage); consumers can not get the quantity of item they desire

Price ceiling: found below equilibrium; occurs when the government puts a legal limit on how high the price of a product can be (ex. rent control)

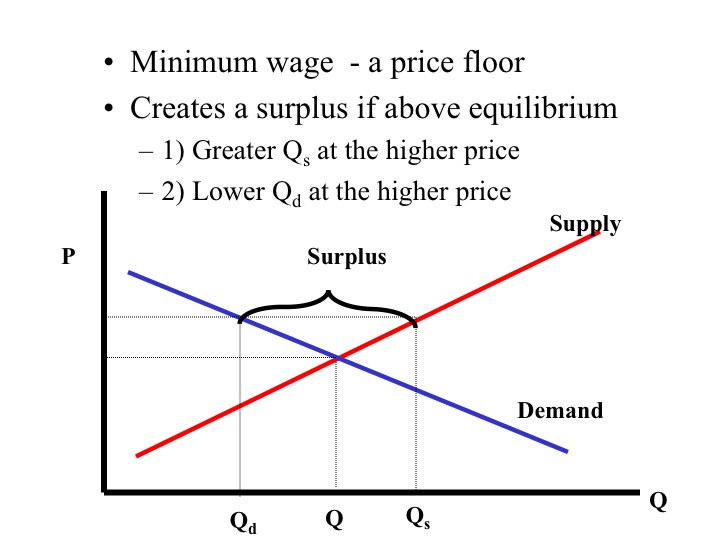

Price floor- lowest legal price of a commodity can be sold at used by the government to prevent prices from becoming too low.

QD>QS excess demands (ex.rent) shortage

QS>QD excess supply/ creates a surplus

Is a PPC an up to date representation of a countries economy?

ReplyDeleteYour blog is very well organized and detailed. In regards to the PPG graphs, do you have more examples of when the economy is in recession, or better yet, how the PPG graph shows the shift to recession?

ReplyDelete