Elasticity of Demand: A measure of how consumers react to a change in price

Elastic demand

1.demand that is very sensitive to a change in price

2.product is not a necessity

3.there are available substitutes

4.always greater than 1

ex. soda/steak/fur coat

Inelastic demand

1.demand that is not very sensitive to a change in price

2.product is a necessity

3.little to no substitutes

4.always less than 1

ex. gas, insulin

Unitary elastic

Perfect society/always equal to 1

Total revenue: total amount of money a company receives from selling goods and services

Price x Quantity = Total revenue

Marginal revenue: additional income from selling one or more unit of a good

Fixed cost: it is a cost that does not change no matter how much of a good is produced

Variable cost: it is a cost that rises or falls depending upon how much is produced

TFC + TVC = TC

AFC + AVC = ATC

TFC/Q = AFC

TVC/Q = AVC

TC/Q = ATC

AFC x Q = TFC

AVC x Q = TVC

Marginal cost = new TC - old TC

output = quantity

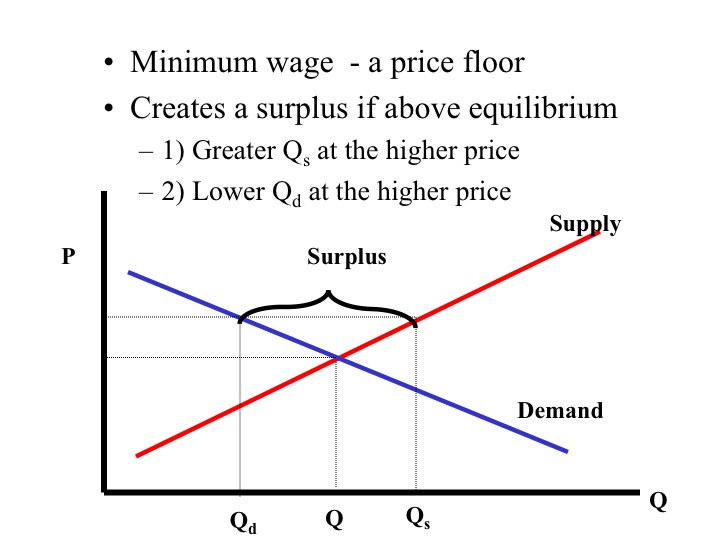

Equilibrium: point at which the supply curve and demand curve intersect

Excess Demand: where quantity demanded is greater than quantity supplied (shortage); consumers can not get the quantity of item they desire

Price ceiling: found below equilibrium; occurs when the government puts a legal limit on how high the price of a product can be (ex. rent control)

Price floor- lowest legal price of a commodity can be sold at used by the government to prevent prices from becoming too low.

QD>QS excess demands (ex.rent) shortage

QS>QD excess supply/ creates a surplus